The rocket flew, the stock popped, and the index is about to do the rest. The fight over the largest IPO in history is not behind us. It is just beginning — and it has to be fought from outside the firm.

Ten days ago Space Exploration Technologies Corp. debuted on Nasdaq in the largest initial public offering in the history of capitalism. The price was not discovered; it was decreed — $135 a share, fixed before the roadshow, take it or leave it. The stock opened at $150 and touched $175, valuing the company at roughly $2.2 trillion, more than Meta. Elon Musk became, on paper, the world’s first trillionaire, and the financial press called it a vindication. It was nothing of the kind. A first-day pop does not prove a price was right; it proves the marketing worked. PetroChina popped too. Facebook popped, then left the investors who bought its IPO underwater for fifteen months.

The question I posed before the offering — should workers’ capital buy into the SpaceX IPO? — has not expired with the debut. It has changed shape. The trustees of public-sector pension systems and jointly trusteed union plans are no longer deciding whether to place an order. Within days, Nasdaq’s rewritten index rules will pull SPCX into the Nasdaq-100, and the decision will be made for them: every index fund, every target-date vehicle, every teacher’s 403(b) that tracks the market must then buy this stock automatically, in proportion to a market capitalization that was itself manufactured. The American Federation of Teachers, whose 1.8 million members participate in funds holding some $3 trillion, took the unprecedented step of asking the SEC to scrutinize the deal, warning of “forced investment.” They were right. What is coming is not an investment decision at all. It is a conscription.

So the post-IPO question is not whether to buy. It is what labor and the progressive shareholder-activist movement should do now that the buying has been taken out of their hands. To answer it, I want to return to a piece of theory I worked out in the Cambridge Journal of Economics some years ago — because the SpaceX structure is not an aberration. It is the purest illustration yet of the problem that theory was built to name.

The governance option, and why it is missing here

Begin with the firm itself. The dominant theory of the corporation, descended from Berle and Means and refurbished by the agency-cost school, rests on a comforting premise: ownership and control are separate, managers are mere agents of dispersed shareholders, and any manager who misallocates capital is disciplined by the “market for corporate control.” Capital markets, on this view, are neutral plumbing that converts millions of buy-and-sell decisions into legitimate outcomes. I argued, following Christos Pitelis, that the picture is false at its foundation. There was no managerial revolution. Capitalists did not surrender control when they sold shares to outsiders; they kept it, commanding socialized labor and social resources from a minority economic stake. The firm is not plumbing. It is an island of conscious power — and once you see it that way, a problem the orthodox account cannot handle appears: legitimacy. The people on the receiving end of corporate power, workers as employees and as the ultimate owners of pension capital, will eventually want a say in whether its outcomes are legitimate. Securities law, fiduciary duty, and shareholder rights are the residue of earlier moments when they demanded one.

The orthodox defense leans on a single load-bearing assumption Pitelis called perfect substitutability: that a worker who dislikes how a company behaves can simply sell. But pension beneficiaries cannot easily sell. They have no control over, and often no knowledge of, the shares bought in their name; they cannot move fluidly between consumption and investment the way the theory requires. They are involuntary investors — hostages to the decisions controlling capitalists make about corporate profits. Their “exit” is largely a fiction, and when exit goes dark, the price signal that is supposed to discipline managers goes dark with it. Absent some other intervention, workers’ deferred wages are quietly “put” back to the capitalist class as capitalist savings — fuel for accumulation, deployed by others, in others’ interests.

What is the other intervention? I called it the governance option. A share is a bundle of rights. Hedge-fund activists care about one strand, the right to payouts; but the bundle also contains governance rights — to vote on major decisions, to obtain information, to speak at the annual meeting, and to bring derivative claims against directors who loot the company. These are an embedded option, and for decades pension funds let it lapse, delegating their votes to Wall Street managers who, dependent on corporate relationships, reliably sided with management. The option expired unexercised, like a weapon never drawn. Labor’s contribution over the last two decades has been to start exercising it: at Tesla, where the CtW Investment Group and allied funds forced board changes; at Facebook, where union-led plaintiffs sued and made Zuckerberg withdraw a plan for non-voting Class C shares. Exercised collectively and credibly, the governance option is the one tool that lets non-controlling owners push back against the private power concentrated inside the firm.

Now look at the SpaceX prospectus with that framework in hand, and you can watch each strand of the bundle being severed in advance.

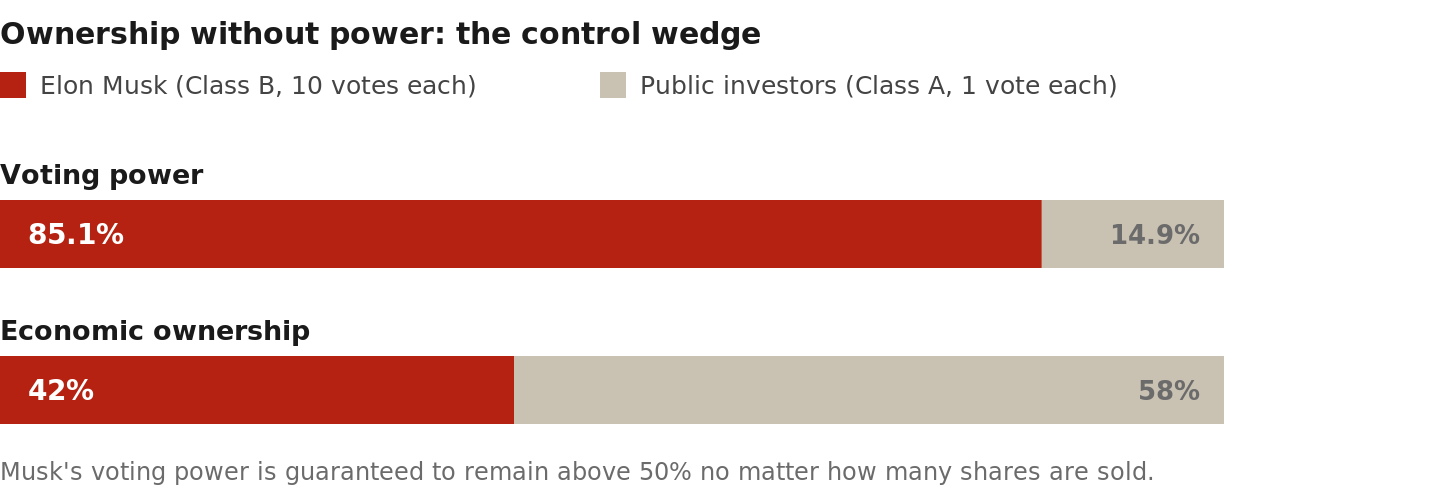

The vote is decorative. Public buyers get one-vote Class A shares; Musk’s Class B shares carry ten votes each. He commands 85.1% of the votes on 42% of the economics — permanently. He can be removed only by a Class B vote he himself controls. Source: SpaceX final registration statement.

The vote is hollow: 85.1 percent of the voting power sits with the founder, locked above a majority forever. The derivative suit — the remedy by which shareholders have policed self-dealing since the nineteenth century — has been priced out of existence. SpaceX reincorporated in Texas in February 2024, days after Delaware’s Chancery Court struck down Musk’s Tesla pay package, and Texas supplies a statute requiring a 3 percent stake before a shareholder may bring a derivative claim — more than $60 billion at today’s valuation, more than any pension system on earth holds in any single stock. The rights to informationand to voice at the annual meeting are nominal in a company whose board is a closed circle of the founder’s friends and co-investors; the “controlled company” exemption strips away even the usual independent-board requirements.

In other words, the SpaceX structure does not merely exploit a lapsed governance option. It is engineered, in advance, so that there is no option left to exercise — the embedded rights emptied out before the first share changes hands. Then, with index inclusion, the last strand, exit, is severed too. This is imperfect substitutability taken to its limit: workers as maximally hostage investors, unable to refuse the purchase and unable to sell, holding a security stripped of voice and of legal remedy. Participation without consent, exposure without voice. That is not a market relationship. It is tribute.

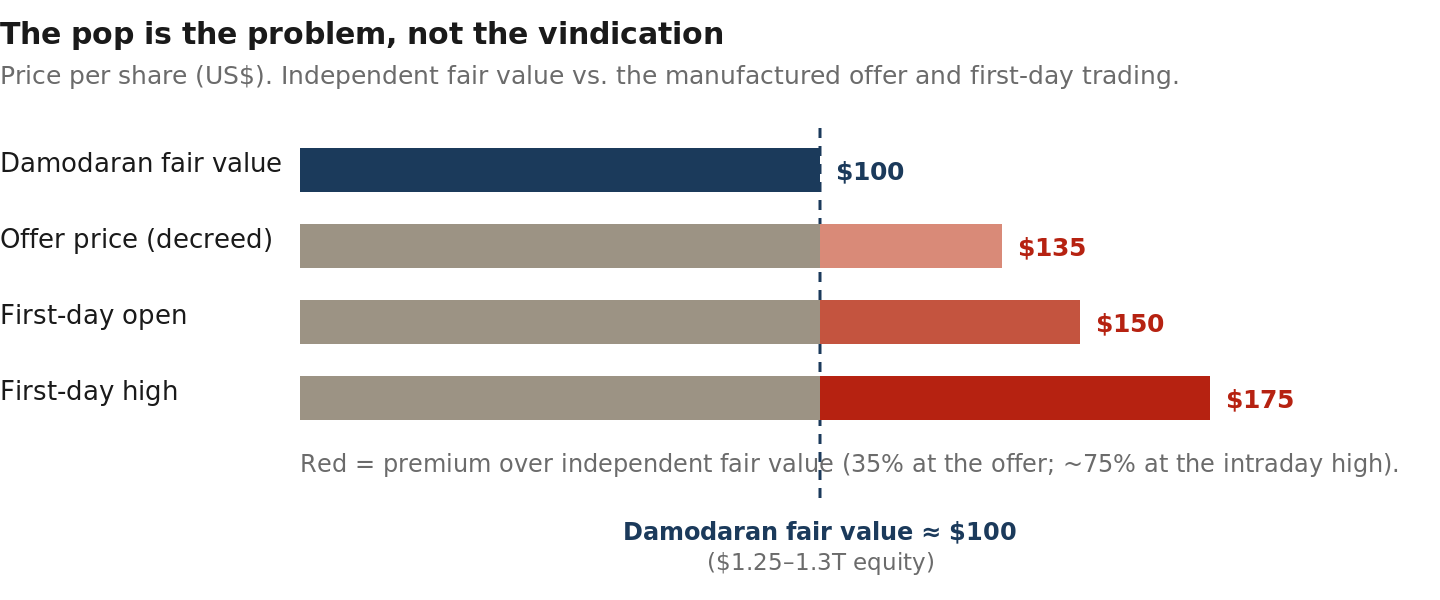

A great company can still be a terrible security. NYU’s Aswath Damodaran — the nearest thing American finance has to a neutral arbiter — values the equity near $100 a share using assumptions he calls generous. The prospectus asserts a $28 trillion “total addressable market,” $26 trillion of it AI; he judges that figure to “border on fantasy.” Sources: Damodaran post-prospectus analysis, June 4, 2026; SpaceX prospectus.

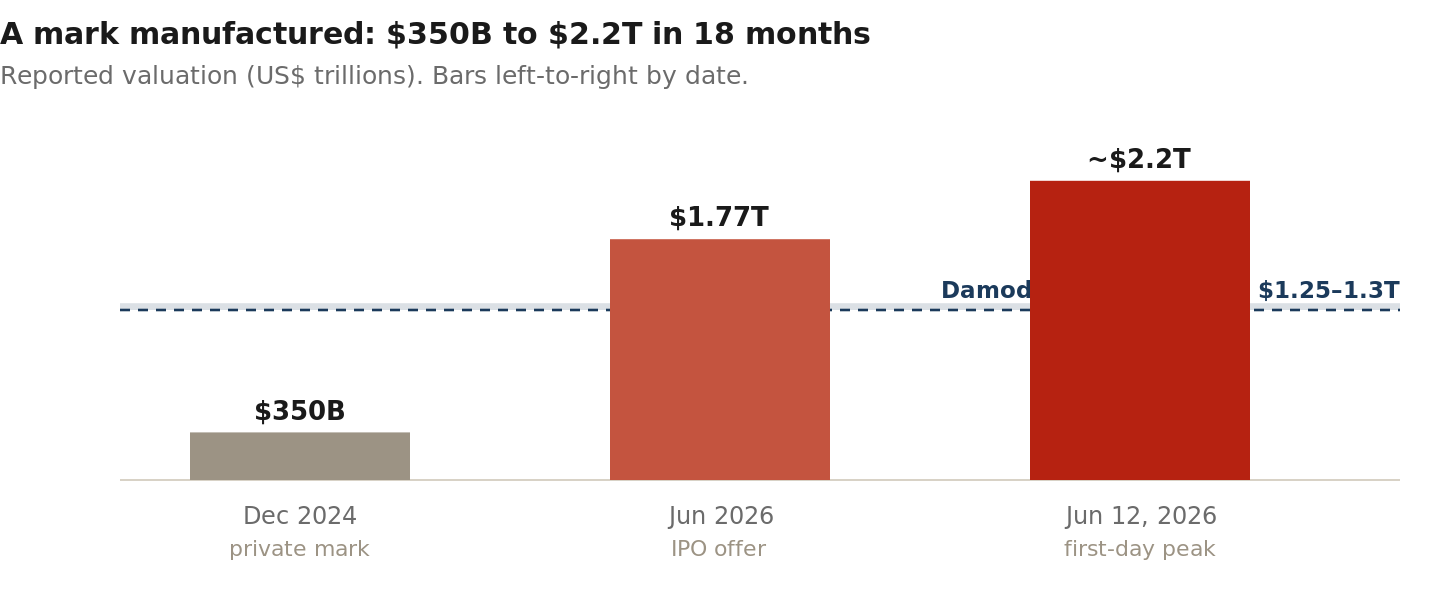

How did a $100 security come to be priced at $135 and trade at $175? Not through discovery. SpaceX was marked at $350 billion in December 2024; fourteen months later the figure was $1.25 trillion — a step-up built on tiny secondaries to obscure offshore vehicles, with undisclosed parties on both sides, and the $250 billion absorption of xAI, a Musk-controlled company bought by a Musk-controlled company. That this was a deal Musk negotiated, in effect, with himself is not my characterization alone; it is how independent observers described the transaction. The IPO was the first arm’s-length price test of this security in years; its buyers were not relying on price discovery but performing it, with their own money.

What independent observers said about the deal

“Musk negotiates with himself, sets the terms, and outside shareholders absorb the risk… the vehicle for value creation is not actual business performance—it’s Musk shuffling assets between entities he controls and stamping a higher valuation on the combination.”

— Fred Lambert, Electrek, May 27, 2026, on the $250B SpaceX–xAI dealOf the earlier xAI–X combination that set the template, William Cohan asked whether “any bankers [were] hired to value the two companies and set an exchange ratio” or whether “special committees of the boards of directors [were] set up to… make sure it was fair to the non-Elon shareholders.” Bloomberg’s Matt Levine judged the valuation “not clearly validated by arm’s-length transactions with economically motivated counterparties.”

— quoted in Mike Masnick, “The X/xAI Shell Game: When Musk Merges With Himself,” Techdirt, April 7, 2025And on what the structure leaves for outside shareholders, NYU’s Aswath Damodaran found in the prospectus “a voting share structure that locks in Elon Musk’s control of the company, since there is little that shareholders can do to restrain the company.”

— Aswath Damodaran, “Revisiting the SpaceX Valuation,” June 4, 2026

The valuation outran any independent estimate of value. The step-up rested on thin secondary trades with undisclosed counterparties and the $250B absorption of xAI — a deal independent observers described as Musk negotiating “with himself” (Electrek; Techdirt). Sources: SpaceX prospectus; reported December 2024 mark; Damodaran, June 2026.

Why “engage from the inside” cannot be the answer this time

The sophisticated counsel inside the labor-investment world says: engage. This is the first of a wave — OpenAI and Anthropic will follow — and a movement that spent four decades building credibility cannot sit out the defining transaction of the era. Better to enter in coalition, with published conditions, and fight from within, as we did at Tesla. I helped build that engagement tradition and respect its instincts. But engagement presupposes channels of influence, and this issuer has closed every one in advance. We ran the experiment: in 2016 CtW’s funds and allies, managing some $700 billion, warned Tesla’s board about the SolarCity related-party deal; in 2018 I took the floor of its annual meeting and urged shareholders to vote against Musk’s captive directors. Engagement under Delaware law, with courts and derivative suits still available, yielded redomestication to Texas and a bigger pay package. SpaceX offers strictly worse terrain — no vote that counts, no court a pension fund can afford to reach, no independent board, and now no exit. A condition-based strategy with no enforcement mechanism is not a strategy. It is a press release with a wire transfer attached.

If the governance option has been emptied inside the firm, then the response cannot be conducted inside the firm. It has to push on the boundary of the firm from outside — what Engels, in a passage I have always found startlingly contemporary, called the invading socialist society pressing inward against the wall of private appropriation. The good news is that labor has done exactly this before, and it worked.

The PetroChina campaign taught that even at the heart of the financial system, organized refusal from below can reprice a deal and rewrite a rule. The stakes now are larger — because the capital being requisitioned is labor’s own.

In 2000, a Goldman-led syndicate set out to float PetroChina on the New York Stock Exchange and hoped to raise $10 billion. The AFL-CIO, joined by human-rights and religious organizations, mounted an “alternative roadshow” that trailed the underwriters city to city, and the deal was slashed to under $3 billion. It left a regulatory residue too: in the 2001 Unger Letter, the SEC conceded for the first time that an issuer’s human-rights conduct could be material to investors — proof that the wall between “financial” and “social” information is not a fact of nature but a political settlement, open to renegotiation. That is the model, scaled up for the age of the trillion-dollar founder. Here is what it looks like now.

An agenda for the post-IPO fight

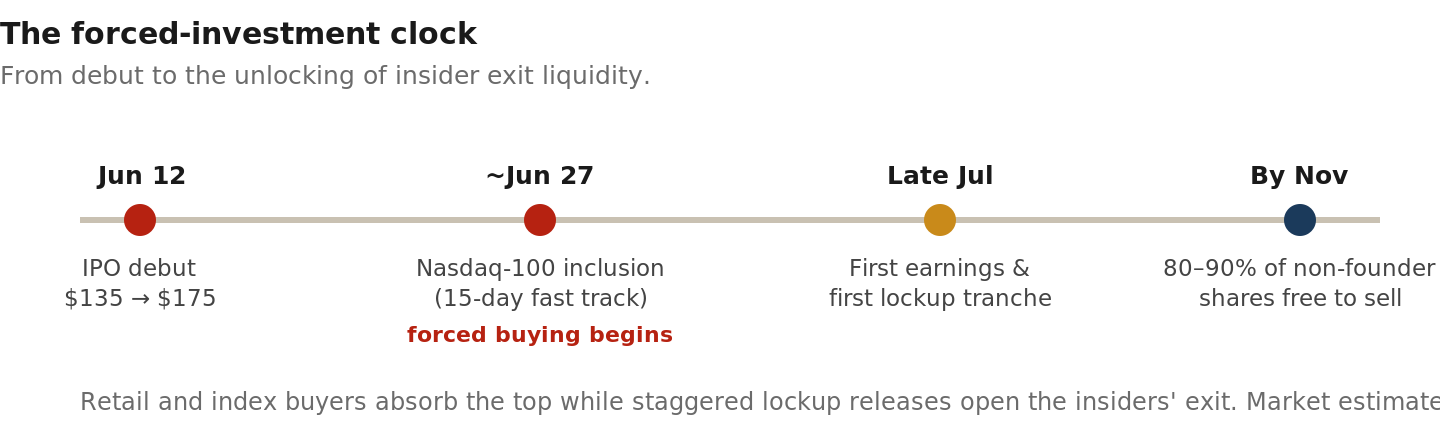

1. Move the fight to the index layer—the new frontier of the exit problem.

This is where the forced-investment fight will be won or lost, and it is the most urgent item on the clock. The mechanism that strips workers of exit is no longer the trading desk; it is the index committee. Reuters reported that SpaceX made fast-track inclusion a condition of listing, and Nasdaq rewrote its rules so a mega-listing can enter the Nasdaq-100 in fifteen days instead of months. Labor should contest fast-track inclusion directly and press the broader principle the moment demands: that benchmark providers adopt governance standards excluding — or weighting down — securities with no meaningful vote and founder lock-in, as index families have restricted multi-class structures before. And trustees should reassert that they never delegated their fiduciary judgment to an index committee’s rulebook. “The index made us buy it” is an abdication, not a defense.

Conscription, then exit. Index funds are forced in just as insider lockups begin to release. Insiders who put less than $11 billion of equity into the company over its lifetime sell into the enthusiasm of the people who cheer the rockets. Sources: Reuters; market lockup estimates; SpaceX prospectus.

2. Rebuild the governance option through law and disclosure, not boardroom diplomacy.

If the rights inside the share have been emptied, refill them from outside the firm, through the regulatory and legal channels engagement bypasses. That means a coordinated wave of SEC comment letters pressing the questions the prospectus finesses: the roughly $205 billion of goodwill atop a subsidiary whose eleven co-founders have all departed; the Starlink unit economics that fell from $99 to $66 in monthly revenue per subscriber while the valuation tripled; the $28 trillion addressable-market claim. It means building, on the PetroChina/Unger foundation, the materiality case that governance and labor conduct are financial facts, not soft “social” ones. And it means treating the Texas 3-percent derivative threshold as a target for litigation and legislative reform — a remedy priced out of existence, not constitutionally abolished.

3. Reclaim the option from the intermediaries who keep “putting” it back to management.

The governance option lapses because pension funds delegate their votes and stewardship to Wall Street managers whose business depends on cordial relations with the very insiders they are meant to police. The largest index providers will be among the biggest holders of SPCX, and their voting policies will matter more than any single fund’s. Labor’s task is to build independent stewardship capacity — in-house proxy voting, shared voting platforms among allied funds, public guidelines that refuse to rubber-stamp controlled-company structures — so the option is exercised by the beneficiaries’ representatives rather than surrendered on their behalf. An option never exercised loses its credibility, like a weapon never drawn; a credible threat changes behavior before it is used.

4. Unite the two roles: workers as owners and workers as employees.

SpaceX is not merely an overpriced, unaccountable security. It is the company that sued to have the National Labor Relations Board declared unconstitutional after firing workers who criticized Musk — and won by attrition this February, when a hollowed-out Board abandoned its case. Reuters has documented more than 600 worker injuries at its facilities, including amputations and a death. The proposition put to a union trustee is therefore obscene on its face: hand the deferred wages of union members, at a 35-to-75 percent premium to fair value, to a company dismantling the legal regime under which those same members organized — in exchange for a share with no vote, no court, and no board. The old worry that prudence and solidarity might conflict dissolves here; they point the same way. Owner-side and worker-side institutions should run this as one campaign, not two.

5. Refuse loudly, on the record, and be candid with beneficiaries about why.

Finally, the alternative roadshow for the age of the trillion-dollar founder: a documented, public, rigorous refusal. Restricted lists. Written-justification requirements for any manager who wants in over a fund’s own benchmark. And honest communication with the teachers, firefighters, and nurses whose savings are at stake — not squeamishness about rockets, but a refusal to let workers’ own capital finance a structure built to be unaccountable to them in both of their roles. The objection was never that the rockets do not fly. Launch margins near 67 percent and Starlink subscribers doubling to 10.3 million are real. A great company can still be a terrible security, and an unaccountable one can still be a political defeat.

Step back and the historical shape comes into view. The postwar settlement bought social legitimacy with institutions — bargaining, social insurance, enforceable rights — that gave the working class procedural standing. The neoliberal era stripped those away and offered a substitute: the worker as shareholder, the pension fund as each citizen’s stake in capitalism’s success. The SpaceX offering abolishes even that bargain’s formal terms — no meaningful vote, no court, no independent board, and now, through index capture, no exit and no entry decision either. A system that must conscript its own working class’s savings while litigating to dissolve that class’s last statutory protections is not generating legitimacy. It is running down reserves accumulated in an earlier age, and the deficit is compounding.

The price is set; the stock has popped; the index will do the rest. None of that settles the question the workers’-capital movement has always posed — whether the class that produces society’s resources will have any say in how they are deployed. The governance option has been emptied inside this firm. So it must be exercised against the structure from outside: at the index committee, at the SEC, in the legislature, and in public. The point was never to catch the biggest deal in history. The point is to contest it.

Stephen F. Diamond is a corporate and securities law scholar who has advised union pension funds for three decades, including the AFL-CIO’s PetroChina IPO campaign (2000) and the CtW Investment Group’s engagements with Tesla’s board (2016–18). The argument here develops the framework of his article “Exercising the ‘governance option’: labour’s new push to reshape financial capitalism,” Cambridge Journal of Economics 43, no. 4 (2019): 891–916. Valuation figures draw on Aswath Damodaran’s June 2026 analysis and the SpaceX registration statement; first-day trading, lockup, and index-timing figures reflect reporting as of June 22, 2026.

A Powerpoint summary of this post can be found here: Should Workers Capital Buy Into the SpaceX IPO (deck).